Fitness Ventures Buys 22 Crunch Gyms: The Operator Read

Fitness Ventures just became the largest single franchisee in the Crunch Fitness network. The company acquired 22 locations in one transaction, a move that instantly redraws the competitive map inside one of the US low-cost gym market's most recognized brands. If you're operating a gym franchise right now, this deal is worth understanding in detail.

This isn't an isolated event. It's a data point in an accelerating pattern of intra-brand consolidation that's reshaping how the high-volume, low-price segment operates at the local level.

What the Deal Actually Signals

The Fitness Ventures acquisition isn't just about scale for scale's sake. It reflects a calculated read on where margins are heading in 2026 and which operators are best positioned to survive the compression. Acquiring 22 units in one move does something that organic growth cannot: it eliminates transition risk, locks in territory, and delivers immediate operational leverage.

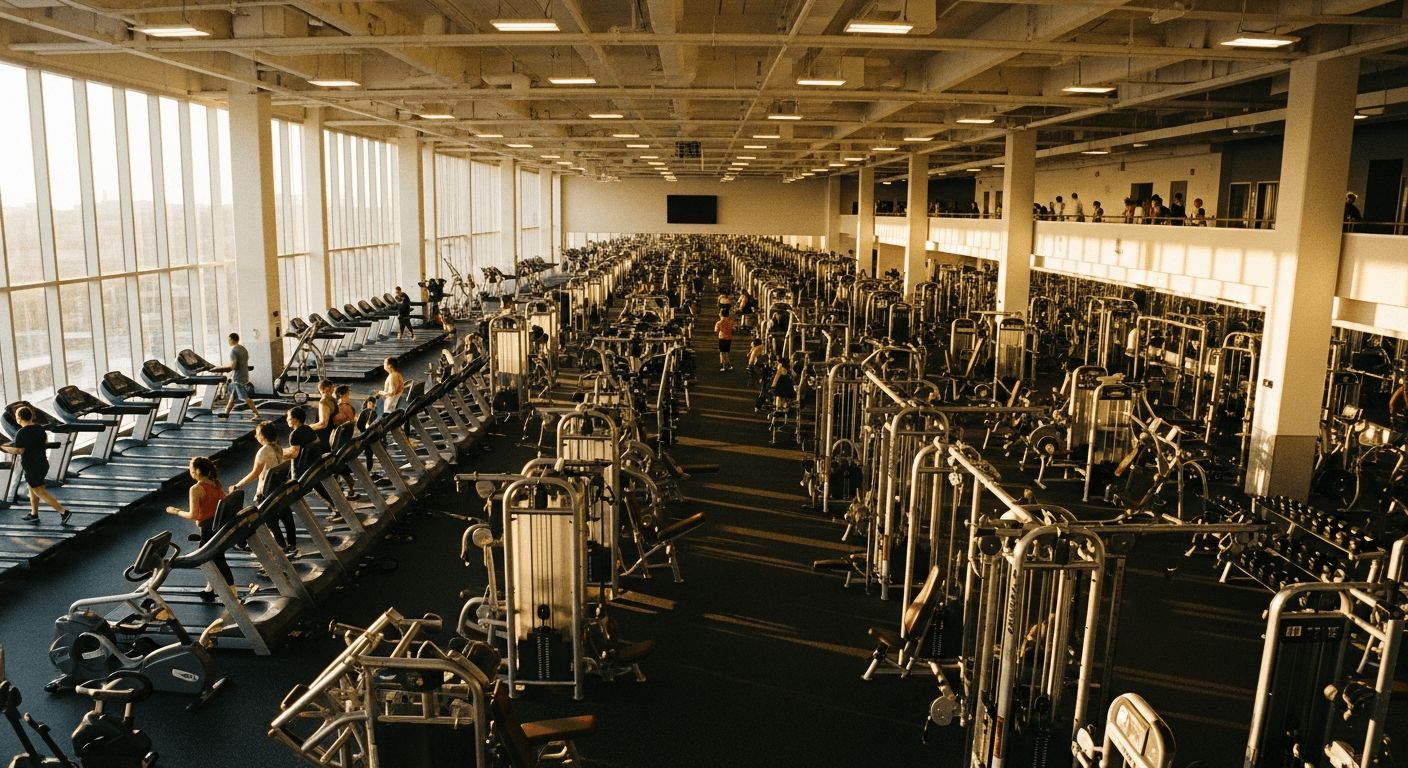

For context, Crunch Fitness has grown to over 400 locations across the US and internationally. A single franchisee now controlling roughly 5% of that network commands a different conversation with corporate than any operator running three or four clubs. That asymmetry matters more than most operators acknowledge.

The broader M&A compression happening across the low-cost gym segment in 2026 is well documented. As Gym Franchise Consolidation 2026: What the M&A Wave Means for Operators outlines, deal velocity has increased significantly as smaller operators face rising costs and limited access to capital on competitive terms. The Fitness Ventures move fits squarely inside that wave.

The Economics of Multi-Unit Scale in Gym Franchising

Here's where it gets concrete. When you operate 22 locations under one entity, the unit economics shift in ways that single-location and small-cluster operators simply can't replicate through effort alone.

The advantages compound across several dimensions:

- Supplier and vendor leverage: Equipment maintenance contracts, cleaning services, software licensing, and energy procurement all carry better per-location rates at volume. A 22-unit operator negotiating a gym management software contract pays a fundamentally different price than a three-unit operator does.

- Staffing and management infrastructure: Regional management layers become economically viable. A single area director overseeing six to eight clubs drops the effective overhead per location below what a standalone operator running one club can achieve.

- Marketing efficiency: Brand spend, digital advertising, and local SEO campaigns spread across a larger member base. Cost per acquisition drops as the denominator grows.

- Territory control: Large franchisees often secure preferred right-of-first-refusal on adjacent territories, making organic expansion cheaper and faster than building from scratch.

The result is a structural cost advantage that doesn't require the small operator to make any mistakes. The gap simply widens over time as scale compounds.

Planet Fitness Confirms the Segment Is Holding

One question worth asking: is this consolidation happening because the HVLP (high-volume, low-price) model is struggling, or because it's worth owning at scale? The evidence leans clearly toward the latter.

Planet Fitness reported continued visit growth and steady per-location demand in early 2026. The $10 to $25 monthly membership price point remains one of the most defensible positions in consumer fitness. Member churn, while never zero, is structurally lower in this segment than in boutique formats where monthly fees can run $150 to $250 or more. When household budgets tighten, the low-cost gym membership is one of the last discretionary items to go.

That resilience is precisely what makes large-format HVLP locations attractive acquisition targets. You're not buying a turnaround. You're buying a proven cash-flow model and adding operational leverage on top of it.

The demand side of this equation also benefits from a broader cultural shift toward consistent training habits. Concepts like zone 2 cardio and structured strength programming have moved from elite athletic circles into mainstream gym culture. Zone 2 Training: What It Is, Why It Works, How to Do It captures how this training methodology has entered the general fitness conversation, driving steady treadmill and cardio floor utilization across large-format gyms.

The Rollup Playbook Inside a Single Brand

What makes the Fitness Ventures deal notable is where the consolidation is happening: inside a single franchise brand, not across brands. Until recently, most gym rollup activity involved private equity firms aggregating studios across formats, or European operators like Basic-Fit, Gym Group, and McFIT scaling regionally through owned corporate locations.

The US franchise model is now running its own version of that playbook. Aligned Fitness Hits 61 Studios: The Boutique Rollup Playbook documented how this logic is already operating in the boutique segment. The Fitness Ventures move shows it translating directly into the large-format franchise space.

When one franchisee reaches this scale within a brand, the dynamic inside the franchisee network changes. Corporate relationships, co-op advertising structures, and even informal influence over brand-level decisions all shift toward the largest operators. Smaller franchisees within the same brand increasingly find themselves operating in a competitive and political environment shaped by players with fundamentally different resources.

If you're running two or three Crunch locations and your largest co-franchisee now operates 22, you're not competing in the same game anymore, even if you share the same brand name above the door.

What This Means for Independent and Small-Franchise Operators

The signal here is direct. Margin compression from technology, labor, and energy costs is not easing in 2026. Software platforms for member management, access control, and retention analytics carry real costs. Labor markets in fitness remain tight for qualified personal trainers and facility managers. Energy overhead for large-format clubs with extensive lighting, HVAC, and equipment loads is significant and rising.

For operators who haven't yet built the scale to absorb these pressures, the timeline to a strategic decision is shortening. The options remain what they've always been, but the urgency around each has increased:

- Scale: Pursue additional locations aggressively, either through organic growth or by acquiring neighboring franchisees who are already considering an exit. The window for acquiring distressed or underperforming units at reasonable multiples is open now and will narrow as larger operators become more active buyers.

- Specialize: Double down on a differentiated member experience that large multi-unit operators structurally cannot deliver. This means coaching quality, community density, and programming specificity. Data-Led Gym Retention: Turn Engagement Signals Into Revenue outlines how operators at any size can use engagement data to build retention that scale alone doesn't produce.

- Exit: If neither scaling nor specialization is viable given your capital position or operational bandwidth, selling to a consolidator now, before further margin erosion, often produces a better outcome than waiting.

None of these paths are easy. But the consolidation signal makes the cost of indecision higher than it was two years ago.

The Broader PE and Franchise Context

It's worth placing the Fitness Ventures deal inside the wider capital environment. Private equity involvement in fitness franchising has matured significantly. Early PE plays in the sector focused on platform building across brands. The current phase is more surgical: identifying franchise systems with proven unit economics and accelerating consolidation within those systems.

The European HVLP models demonstrated the ceiling of this approach at the corporate chain level. Basic-Fit operates over 1,300 locations across Europe. Gym Group and McFIT have run similar high-density low-cost playbooks across the UK and German markets respectively. The US franchise structure, with its distributed ownership model, delayed this consolidation phase. It's now arriving.

For operators interested in understanding how PE capital is reshaping the broader fitness landscape, PE and Boutique Fitness: What Operators Must Know Now provides a detailed breakdown of how capital is being deployed and what it means for both boutique and large-format operators navigating this environment.

The Competitive Reality at the Local Level

Ultimately, franchise consolidation plays out club by club, market by market. When Fitness Ventures absorbs 22 locations, it brings unified management, marketing, and operational systems to clubs that were previously run by different operators with different levels of investment and capability.

That standardization can improve member experience in previously underperforming clubs. It can also mean that local operators who were competing against a less-resourced Crunch franchisee now face a much more professionalized competitor under the same brand.

The most important thing you can control as an operator is your own unit economics and your member relationship quality. Scale deals change the competitive landscape. They don't change the fundamentals of why members stay, refer others, and pay consistently. Building on those fundamentals is the most durable response to a consolidating market, regardless of what the largest operators in your segment are doing.

The Fitness Ventures deal is a clear signal that consolidation inside franchise brands is accelerating. If you're running a gym in 2026, the question isn't whether this trend is real. The question is what you're doing about it before the next deal closes in your market.